Asian buyers to help return sparkle to fine jewellery and watch market crippled by COVID-19

share on

With combined annual sales of over US$329 billion in 2019, as estimated by McKinsey, fine jewellery (US$280 billion) and watches (US$49 billion) hold a significant portion of the contribution to global business. However, stunted by COVID-19 conditions, both sectors find themselves at an inflection point.

Fine jewellery and watch industries suffered revenue declines of 10% to 15% and 25% to 30% respectively, according to McKinsey. This was largely due to the closure of physical retail outlets and both the industries’ slow transition to digital — which lags far behind other luxury categories — with online sales representing approximately 13% of the market for fine jewellery and just 5% percent for watches.

While global travel is not expected to return to pre-pandemic levels much before 2024 according to McKinsey, by 2025, there will be an expected increase in demand from younger consumers as well as those shopping domestically, amid continuing restrictions on international travel and the rise of domestic duty-free zones in China.

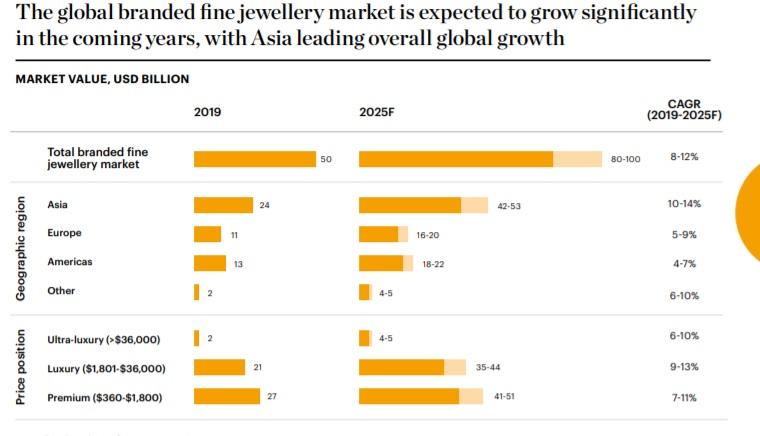

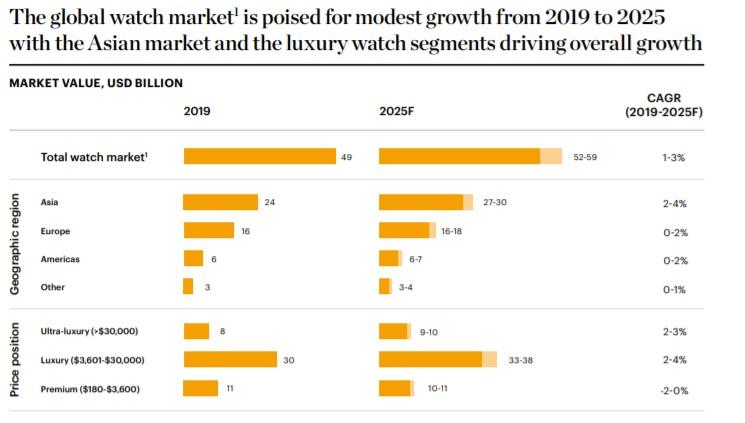

Already the biggest regional market accounting for approximately 45% of branded global fine jewellery sales and approximately 50% for watches, Asia is set to expand its share even further, with China leading the way.

McKinsey added that globally, Chinese consumers will grow in importance for global brands as the centre of gravity for fine jewellery and watches increasingly tilts towards Asia. Accompanied by rapidly growing wealth in the region — the number of households in Asia with incomes above US$70,000 is expected to almost triple by 2025 — the pace of growth for both fine jewellery and watches in the region will remain above the global average each year.

Sales of branded fine jewellery in Asia are expected to grow at a 10% to 14% CAGR between 2019 and 2025 (compared to a global branded jewellery average of 8% to 12%), while watches will grow at a CAGR of 2% to 4% (compared to a global average of 1% to 3%).

Keen on resetting your retail plans? Join our Retail Reset conference to hear from brands such as Robinsons, COMO, Dyson and many others. More here.

With travel between the main shopping regions of Asia, Europe and the United States only expected to fully recover after 2024, the road to recovery for international purchases will be long. In the meantime, domestic purchases are expected to continue to rise and partially fill the void. According to Agility Research, over half of affluent Chinese consumers who bought a watch in the second half of 2020 did so domestically. This will likely boost duty-free shopping hubs like the Chinese island of Hainan, which has benefited from the rise of domestic luxury purchases.

3 trends shaping the jewellery market:

Buying into brands: Despite the prominence of some of fine jewellery’s biggest players, with their iconic brand identities and global reach, sales of branded fine jewellery still account for just 20% of the market. But by 2025, brands are set to take a bigger slice from the unbranded segment, growing to represent between 25% and 30% of the market. Branded fine jewellery is expected to grow at 8-12% CAGR from 2019 to 2025, outpacing the overall fine jewellery market. Those able to convert consumers to branded jewellery will share in the spoils of the collective US$80 to US$100 billion up for grabs.

Online magic: Fine jewellery sales are traditionally associated with a bespoke service and magical in-store experiences that do not easily translate online. With online jewellery purchases surging since the pandemic, the onus is now on brands and retailers to better understand the relationship between physical and digital channels to develop experiences that capture more of the online fine jewellery market. With online sales expected to grow from 13% to 18-21% of the overall market between 2019 and 2025, US$60-US$80 billion are at stake.

Sustainability surge: Fine jewellery purchases influenced by sustainability considerations are poised for dramatic growth. By 2025, an estimated 20-30% of global fine jewellery sales will be influenced by sustainability considerations from environmental impact to ethical sourcing practices. But leaders in a previously slow-to-act industry must look beyond sustainability as a factor in risk mitigation and embrace it as an opportunity to build brand equity by pursuing responsible business practices.

3 trends shaping the watch market:

DTC shakeup: Offline retail has been the life source of the watch industry for decades, with multi-brand retailers owning the customer relationship. But as consumers demand better online shopping experiences and brands aim for higher margins, watchmakers will grow their direct-to-consumer channels and take control of the customer relationship through a dynamic, omnichannel approach, as US$2.4 billion in annual revenues are set to transfer from retailers to brands by 2025. Average annual growth of DTC watch sales is expected to be 7-9% from 2019 to 2025, increasing DTC sales from 20% of overall sales in 2019 to approximately 30% in 2025.

Mid-market squeeze: The traditional mid-market for watches is feeling pressure from both sides. At the entry level there is intense competition from digital natives, fashion brands and the fast-growing smartwatch category, and at the higher end many customers are trading up to luxury. Mid-market brands must revitalise their brand narratives to differentiate themselves, refine their product offerings and create more intimate connections with consumers, or risk foregoing revenues of up to US$2.5 billion by 2025. Market share of the traditional mid-market watch segment is expected to decline by six percentage points from 2019 to 2025 if no action is taken to mitigate competitive forces.

Pre-owned profits: The pre-owned watch market has become increasingly attractive thanks to digitisation, which turned it into the industry’s fastest-growing segment. The market is expected to reach US$29 to US$32 billion in sales by 2025, which will be more than half the size of the first-hand market at the time. Brands must work hard to capitalise on this shift, and digital platforms will need to sharpen their business models in an increasingly competitive environment. Pre-owned watch sales are expected to grow 8-10% annually from 2019 to 2025, increasing from US$18 billion in 2019 to US$29 to US$32 billion in 2025.

share on

Free newsletter

Get the daily lowdown on Asia's top marketing stories.

We break down the big and messy topics of the day so you're updated on the most important developments in Asia's marketing development – for free.

subscribe now open in new window